Factoring Continues to be a Relevant Factoring Instrument in Singapore

Introduction

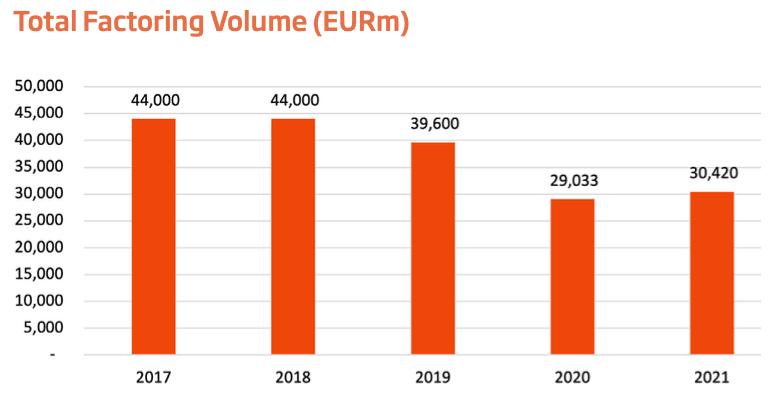

With SMEs accounting for 99 per cent of total enterprises in Singapore and with credit terms being the norm in B2B business dealings, factoring continues to be a relevant financing instrument in Singapore. It is estimated that factoring volume grew five per cent in 2021 to EUR 30.4bn. The financing landscape continues to be a competitive one with the banks, factoring companies and fintechs offering different types of loans and financial products to the SME sector. The factoring industry will continue to see evolution, innovation and digitisation in this economy of ‘the new normal.’

Factoring Industry Environment

With countries around the world gradually reopening in 2021, Singapore’s economy, which is strongly export oriented, expanded by 7.6 per cent during the year. Now, as the country takes steps towards living with Covid-19, the GDP growth forecast for 2022 is being maintained at three per cent to five per cent, according to the Ministry of Trade and Industry.

The manufacturing sector grew by 13.2 per cent, accelerating after the 7.5 per cent growth in 2020. This growth was attributed to a rise in output across all sectors, with the precision engineering, electronics and transport engineering sectors taking the lead. The construction sector expanded by 20.1 per cent, from a dip of 38.4 per cent in 2020, supported by projects from both the public and private sector.

Credit continues to dominate the terms of trade in Singapore. According to the Atradius Payment Practices Barometer 2021, close to 60 percent of domestic B2B sales are on credit and the usual credit terms are 30 days. Trading on credit is used to attract new business (industry norm) as well as to preserve competitiveness in the business arena.

According to the survey 52 per cent of respondents experienced late payment and 24 per cent indicated that they use trade credit as a short term financing tool as well. This indicates that factoring and invoice financing have continued to be one of the relevant financing instruments in funding working capital needs and to increase sales.

SMEs form 99 per cent of total enterprises and 44 per cent of economic output. The number of SME enterprises is growing year on year. Please refer to the table above.

Term loans remain one of the most popular forms of working capital sought by SMEs. An example is the Temporary Bridging Loan program (under Enterprise Singapore) which was set up in April 2020, later extended to 30 September 2021 and then extended further to 30 September 2022. In conjunction with the support of the Monetary Authority of Singapore, this scheme offers low cost financing to qualifying SMEs and since its inception the facility has disbursed SGD 14.2bn to eligible financial institutions to support their lending to companies under the scheme.

SMEs are generally receptive towards factoring given that the terms of trade for B2B sales in Singapore are still largely on credit. Such terms justify the need to access cash early from the receivables to fund business working capital needs. Nonetheless it is believed that the GDP penetration rate of factoring is still low at less than ten per cent. There is much still to be done in this industry to educate SMEs in terms of the benefits that it offers. Some of the concerns SMEs may have with factoring include:

1) High costs of financing

2) Additional work for accounts and administrative staff

3) Massive paperwork and supporting documentation

4) Fear of involving their customers (i.e. debtors) in the process

Hence digitisation and automation are vital to resolve some of these concerns by reducing manual processes (e.g. preparation and submission of invoices, uploading of invoice schedules) in clients’ systems interfaces with factors. Digitisation and automation will also help to reduce the costs of factors which could in turn help them to offer more competitive pricing to their clients. The ability to verify invoices is another critical process to ensure funding can be released swiftly upon submission of invoices. Therefore, a collaborative working arrangement with the buyer (as the debtor to the proposed factoring arrangement) is crucial to ensure a healthy and efficient ecosystem for the suppliers.

Market Performance and Supply

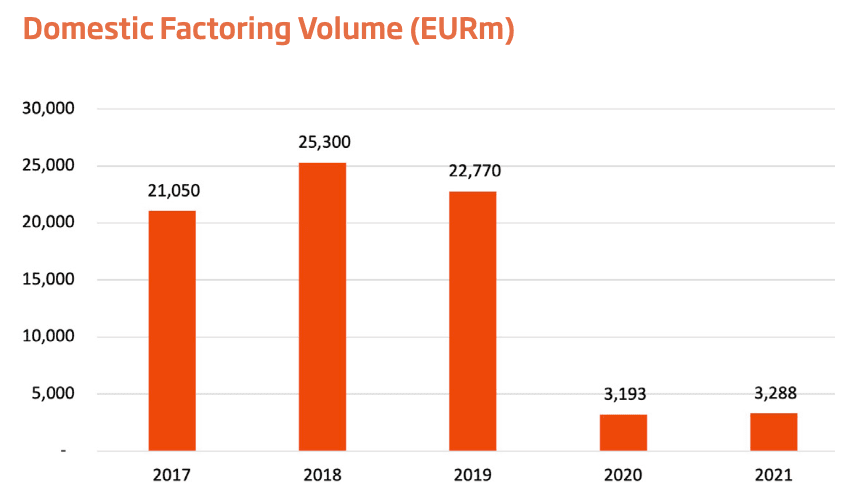

There have been no official figures on factoring volume for 2021. As the economy is still not out of the woods from the Covid-19 disruption, factoring volume has therefore been cautiously estimated to have been EUR 30.4bn in 2021, with growth of five per cent compared to 2020. Domestic factoring volume has been estimated at EUR 3.3bn assuming some recovery in the construction sector and other domestic sectors.

International factoring volume was estimated to have grown by five per cent to EUR 27bn, and derived from the manufacturing sector (e.g. precision engineering, electronics and transport engineering), which expanded significantly in 2021.

There are two segments of factoring clients, SMEs and corporates, where the latter are usually served by the banks. The factorable industries in the SME sector include manufacturing (precision engineering and electronics), labour intensive industries such as construction, engineering and the facilities management sector.

The average client size is typically an annual sales turnover of around SGD 1m to SGD 3m. Facility limits range from SGD 300,000 to SGD 500,000.

Pricing structure differs among different factors, which is determined by their go-to-market strategies. A typical factoring facility would be as indicated in the table below.

The factoring market is still fragmented with the larger and better credit rated SMEs being served by the banks, while the less bankable ones are targeted by factoring companies and fintechs. The major bank players are DBS, UOB and Standard Chartered to name but a few. Non-bank players include factoring companies such as Bibby Financial Services, IFS Capital and fintech lenders such as Funding Societies and Validus. It is noteworthy that most factoring players offer multiple financial products such as unsecured term loans and asset-backed loans, and there is no single focus on factoring alone. This product bundling strategy is to cater to the pre- and post-delivery financing needs of SMEs. While there are no major factoring companies dominating the factoring market, it is estimated that local and foreign banks contributed 90 percent of factoring volume in Singapore in 2021.

In the fintech space the competition has become ever more intense. Southeast Asian SME digital financing platform, Funding Societies, has recently announced the launch of Elevate, a virtual card for micro, small and medium enterprises (MSMEs) in Singapore. This is where qualified MSMEs are eligible for interest-free credit for a period of up to 55 days and for limits under SGD 30,000 with no personal guarantees required. Again, this is an indication of how innovation in the financial services sector is gathering pace and players in the market have to evolve and adapt to remain relevant.

To stay competitive many factoring providers have upped their game to increase or just to maintain their share of the market. Pricing has remained one of the commonest competitive tools, for the providers are not just competing against other factors but also against other types of financing (e.g. term loan which is priced at six per cent to seven per cent p.a., and is usually perceived to be cheaper). Other factors will have to increase client loyalty by improving their customer experience (through ease and speed of access, flexibility in facility structure, and integration with the ecosystem).

Currently there is no known factoring association in Singapore.

Future Trends

Singapore is striving towards becoming a ‘Smart Nation’ that leverages on technology to improve the lives of citizens and business owners. Currently, 95 per cent of all transactions with the government are done digitally from end-to-end. The government is also encouraging and helping SMEs to embrace technology and digitalisation to enhance productivity and to grow in the digital economy. The IMDA's SMEs Go Digital programme is one such initiative where more than 80,000 SMEs have adopted digital solutions from the program. Therefore, factors as service providers in an industry where traditionally paperwork, client and debtor touch points are massive, will have to innovate and digitalise in order to stay relevant in the competition for clients. Automation and digitalisation will not only streamline the whole funding process and enhance customer experience, they will eventually drive down cost which is one of the main concerns of SMEs in embracing the factoring product as a financing tool.

A collaborative ecosystem is essential to sustain the growth of the factoring industry. This involves not only the client of the facility but also the debtor, payment platform, blockchain and any other service provider that could add value to the supply chain. A collaborative and integrated factoring ecosystem ensures that invoices flow seamlessly from submission, verification and approval to funding in the fastest and safest way. Factors cannot control the whole supply chain, but they can certainly collaborate vertically or horizontally across the value chain.

Reach out to Hubble.Financial to learn how you can manage your funds today.

Share this article

Explore Related Content

Stay up to date with our latest news features!

CPD Trade Data for SGBuildex — Mapping, Multi-Skilled Workers, and Mid-Project Changes

Mobile Biometric Check-In for SGBuildex CPD — Open Sites, Space Constraints, and Business Continuity